It is confusing to most of us who do work in real estate whether they be agents or those working in lending retail front, condominium lending guidelines are somewhat ambiguous. A lending source of mine and I hashed it over lunch, it was a good way to mix the less palatable with a savory incentive, food. Anyway, the communication didn't come across clearly or at least I was told that there was a lot of gray matter, no brains mind you, but a lot of stuff left to interpretations. After all as she reminds me, it is a guideline.

Although conventional loans are less restrictive but do require a higher down payment, FHA loans are more restrictive because it is insured by the government and the asset, in this case condominiums which have higher investment risks, requires a small minimum percentage down of about 3 to 3.5%. If you take it from the stance of a tax paying citizen, it's a process we're willing to support and agree to, a necessary process even if it is an inconvenient process for a piece of the American dream of

home ownership.

FHA condo loan requirements include all of the following and but does not include all:

1. At least 51% of the total units must be owner occupied or sold, not rented out.

2. At least 90% of the total units must have been sold.

3. No single entity (i.e. business ownership, or private ownership), may own more than 10% of the total units in the same project.

4. There must be no litigation or legal actions pending.

5. The common areas must be completed with no additional assessments or special assessments separate from that of the

HOA (Homeowner Association) dues.

6. The

HOA reserve fund, independent from operating expenses, must be at least 60% to prevent deferred maintenance (i.e. roofs, siding, plumbing, windows, etc.).

7. Proof of

Insurability, or proof that the building has been and is still insured.

8. Condo projects having more than 30 units, no more than 10% of the units can become FHA approved at any given time. OR if the condo projects having less than 30 units may have no more than 20% of the total units become FHA approved at any given time.

9. There are exceptions and the guidelines can be tailored to fit each projects needs.

Some condo projects may have their building FHA ready - that just means the project has been put through the process, the ringer, to get the entire project qualified for FHA loans. The process has a cost - time. What if the condo complex doesn't have the time or want the inconvenience just to have the entire complex qualify for just one seller? That's where spot approval steps in. It means what it says, on the spot approval. What it doesn't mean is that it will be quick. No surprise there.

Here is a guideline for what a spot approval may look like. Keep in mind that this is an August 1996

exurb from

hudclips.org:

_______ 1. The legal documents of the homeowners association do not contain a right of first refusal or restrictive covenant.

_______ 2. The unit is part of a condominium regime that provides for common and undivided ownership of common areas by unit owners.

_______ 3. The project, including the common elements, and those of any Master Association, are complete, and the project is not subject to additional phasing or annexation.

______ 4. (a) There are no special assessments pending.

______ (b) No legal action is pending against the condominium association, or its officers or directors.

______ 5. The common areas have been under the control of the homeowners association for at least one year.

______ 6. At least 90 percent of the total units in the project have been sold. Verified by _________________________.

______ 7. At least 51 percent of the total units in the project are owner-occupied. Verified by ______________________.

______ 8. There are no adverse environmental factors affecting the project as a whole or individual units .

______ 9. No single entity owns more than 10 percent of the total units in the project. Verified by ______________________.

______ 10. The units in the project are owned in fee simple or the units are held under a leasehold acceptable to FHA.Leasehold in file.

______ 11. The owners association has adequate common area insurance coverage. General liability, replacement coverage,etc. reflects the character, amenities and risks of the particular development. Flood and other insurances carried, when applicable.

______ 12. General maintenance level of common elements is acceptable and there is no deferred maintenance, based on the comments by the Appraiser and/or the pictures.

______ 13. The owners association has a reserve plan and are serve fund, separate from the operating account, that is adequate to prevent deferred maintenance. The amount of the fund is $_________ as of __________.

_______14. (a) For projects consisting of over 30 units, no more than 10 percent of the total units are encumbered by FHA insured mortgages. Verified by ___________________.

_______ (b) For projects consisting of 30 units or less, no more than 20 percent of the total units are encumbered by FHA insured mortgages. Verified by _______________.

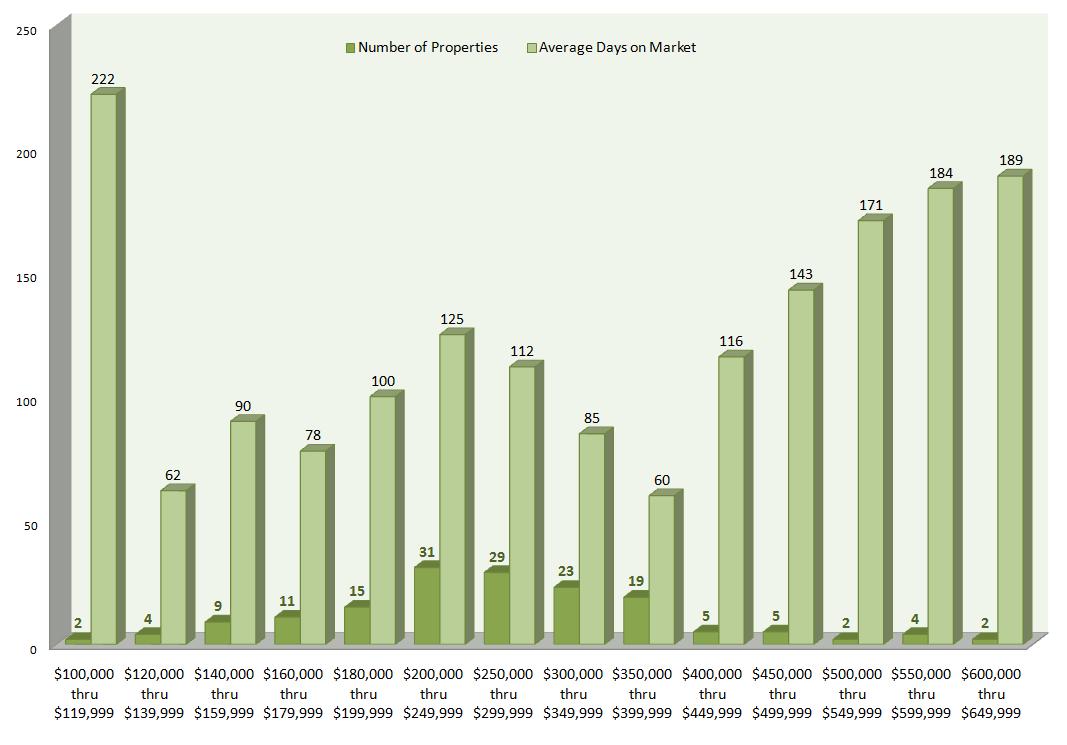

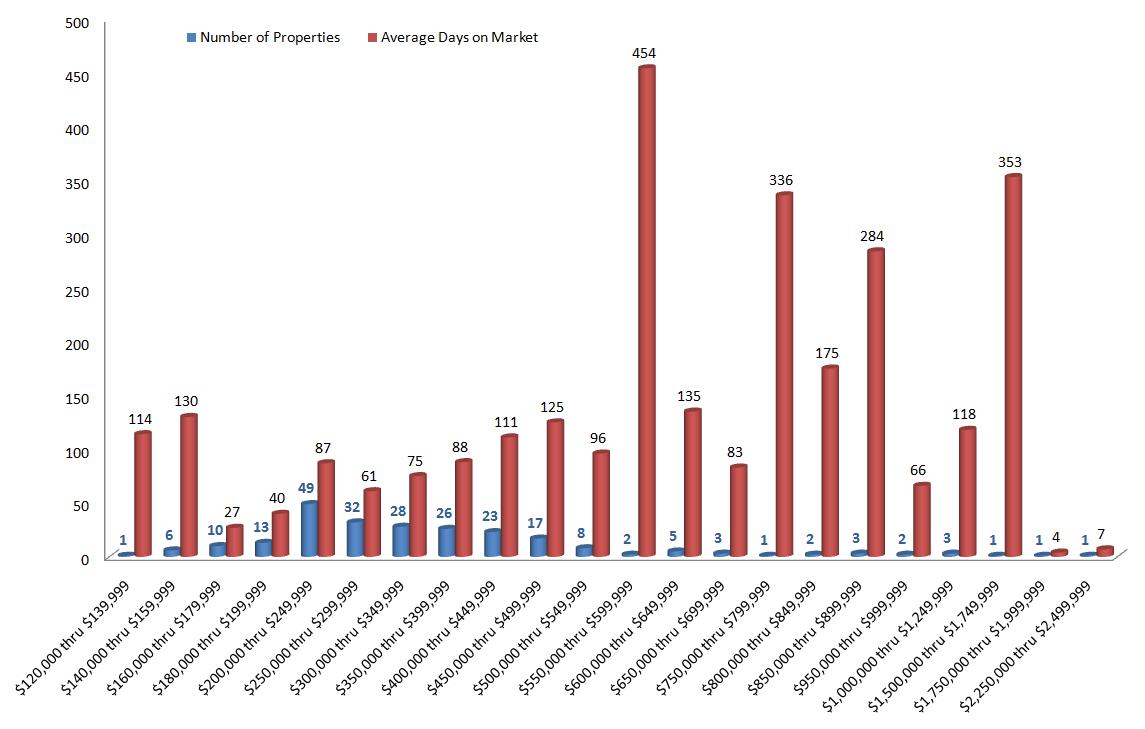

Graph courtesy of

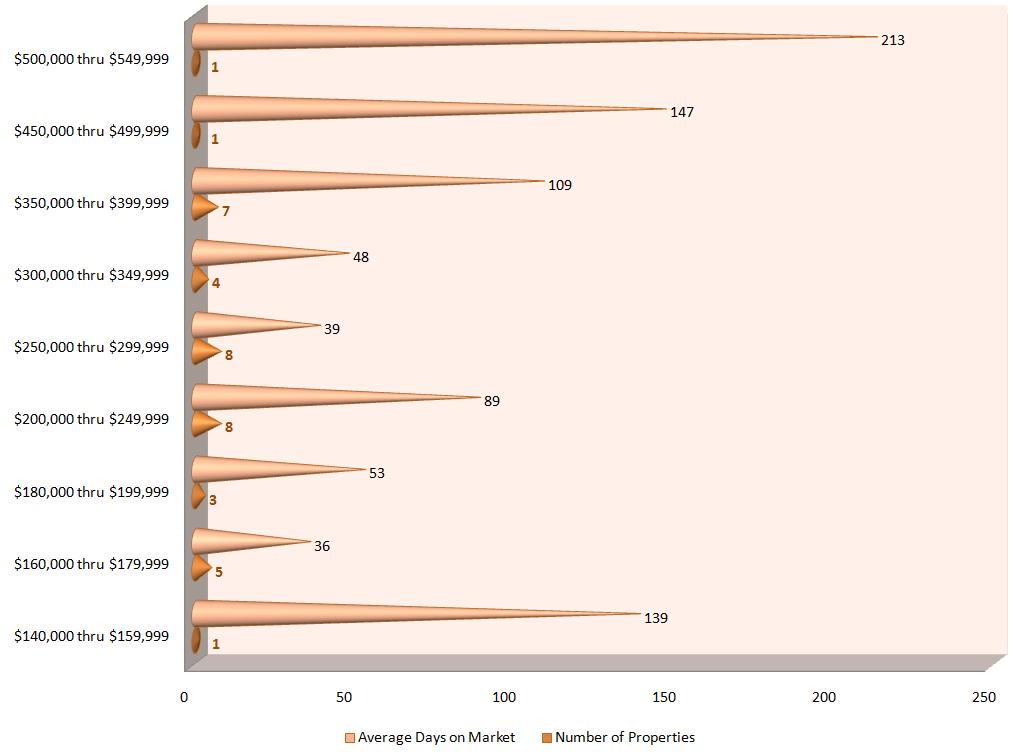

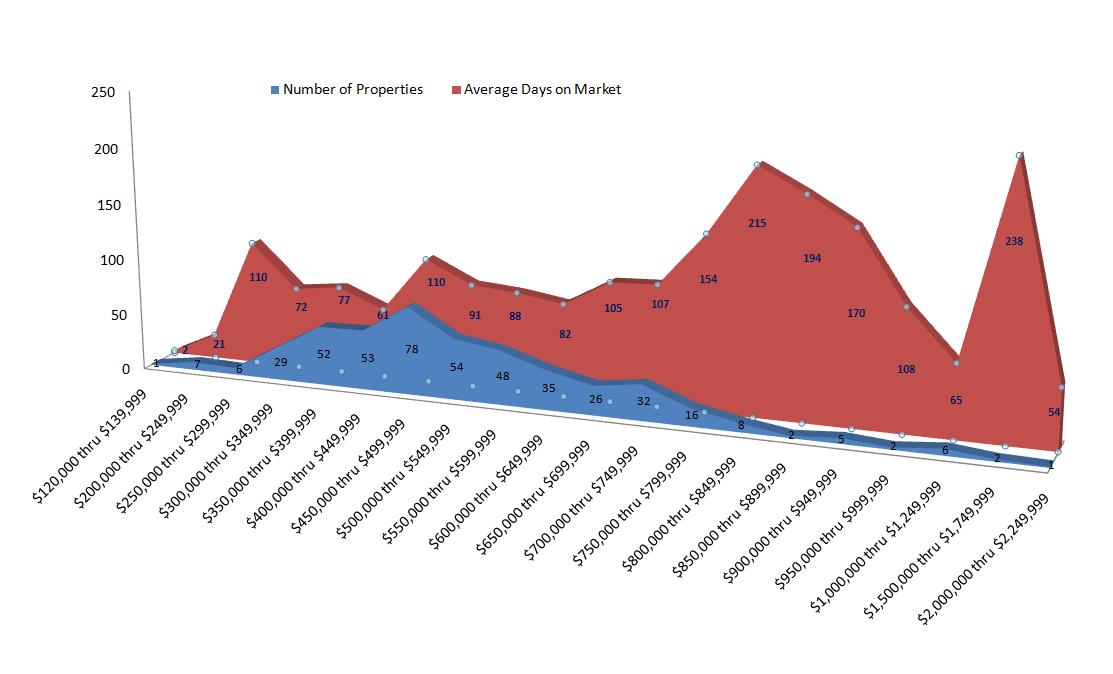

Graph courtesy of

{kind=link}